IR Stock Drops After Big Impairments & Deals

Tue, March 24, 2026Introduction

Ingersoll Rand (NYSE: IR), a leader in air compressors, vacuum systems, blowers and fluid management solutions, saw heightened investor scrutiny this week after a series of company disclosures and trading events. A notable intraday decline combined with large impairment charges and aggressive acquisition activity has reframed the investment debate: is IR’s strategic expansion being priced in, or are integration and end‑market risks eroding value?

What Happened This Week

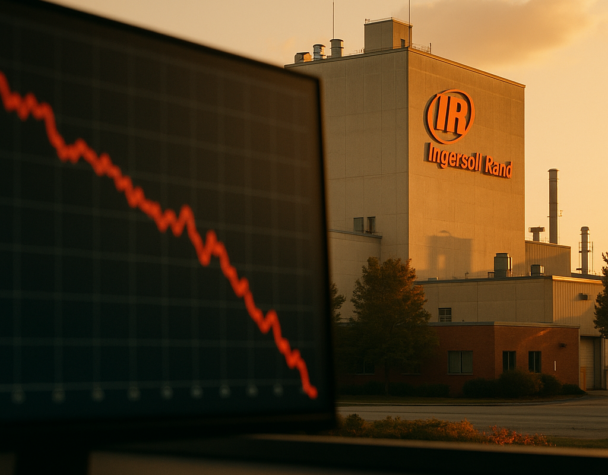

On March 12, IR stock fell roughly 4.7% in a single session amid unusually heavy trading volume—around $270 million—marking one of the firm’s busiest trading days in recent memory. That drop followed public filings revealing substantial impairment charges in the Precision & Science Technologies segment and fresh detail on the company’s acquisition cadence.

Impairments That Matter

IR recorded approximately $229.7 million in goodwill impairment and another $36.1 million against other intangible assets tied to Precision & Science Technologies. These write‑downs reflect softer-than-expected demand and signal that certain acquired units are not meeting previously anticipated performance thresholds. Large impairments like these often act as a red flag for investors because they reveal hindsight revisions to acquisition-related expectations and can compress forward earnings unless management demonstrates meaningful operational recovery.

Active Deal-Making Continues

At the same time, Ingersoll Rand closed nearly $496.1 million in net acquisitions during the latest reporting window, adding businesses such as Scinomix, SSI Aeration and Excelsior Blower Systems. These purchases are intended to broaden IR’s exposure to life‑science automation, aeration solutions and aftermarket blower capabilities—areas that can lift margins and recurring revenue if integrated effectively.

Why Investors Reacted

The market response was driven by several concrete factors:

- Valuation Pressure: IR has been trading at a premium multiple relative to peers, so any hint of execution trouble makes investors reassess upside.

- Impairment Size: The magnitude of goodwill and intangible write‑downs suggests prior acquisition assumptions were optimistic.

- Insider and Institutional Selling: Reports of stake reductions by insiders, including senior executives, and institutional adjustments (e.g., Richard Bernstein Advisors) amplified concern about near‑term confidence.

- Deal Integration Risk: Rapid M&A activity accelerates exposure to cross‑selling, systems alignment and cultural integration risks—areas where missteps can drag on free cash flow.

Balance Sheet and Liquidity Context

Despite these concerns, IR maintains meaningful financial flexibility. The company reported about $2.6 billion of undrawn credit capacity, which supports ongoing integration work and future deal financing. The contrast—solid liquidity versus headline impairments—creates a mixed picture: adequate resources to execute strategy, but increased scrutiny on how those resources are deployed.

Industry Implications: Air Compressors, Blowers and Fluid Management

IR’s moves are strategically logical for its core product lines. Acquisitions like Scinomix expand IR’s foothold in automation and life‑science process equipment, while SSI Aeration and Excelsior strengthen its blower and fluid management capabilities. If executed well, these additions can increase aftermarket revenue, improve product breadth and enhance cross‑sell opportunities across air compressors, vacuum systems and fluid handling solutions.

Execution Is the Differentiator

However, the recent impairments underscore that the value of M&A is realized only through disciplined integration: consolidating supply chains, aligning product roadmaps, retaining key customers and capturing projected synergies. The market is therefore pricing in near‑term integration risk until IR can demonstrate consistent margin expansion and cash conversion from acquired units.

Conclusion

The recent sell‑off in IR stock reflects a reevaluation of risk versus reward as Ingersoll Rand pursues a heavier M&A posture while navigating uneven end‑market demand in certain segments. Large impairment charges have trimmed reported book value and spotlight execution slack, even as the company holds significant liquidity and continues to add strategically relevant businesses. For shareholders and analysts, the near‑term focus will be on integration milestones, cash generation from newly acquired assets, and any additional disclosures that clarify where demand is stabilizing versus where it remains challenged.

Keywords: Ingersoll Rand, IR stock, impairments, acquisitions, air compressors, blowers, fluid management, Scinomix, SSI Aeration, Excelsior Blower Systems.