Fastenal Sales Jump; Reporting Boosts MRO Clarity.

Fri, November 21, 2025Fastenal Sales Jump; Reporting Boosts MRO Clarity

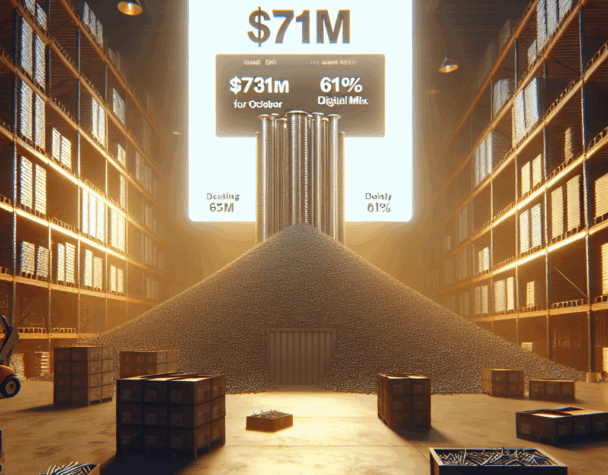

Fastenal (NASDAQ: FAST) delivered a notable October update that combines robust top-line growth with a company commitment to clearer segment reporting. The firm reported $771 million in October sales—an 11.6% increase year-over-year—and confirmed an upcoming change to its financial disclosures that will separate OEM and MRO performance more explicitly. These developments matter to investors focused on industrial supply and maintenance, repair and operations (MRO) exposure because they reduce ambiguity around where revenue is coming from and how durable demand is across end users.

Headline performance: What the numbers show

October’s $771 million in sales represents a meaningful acceleration in aggregate revenue. Digital channels and eCommerce remain central to Fastenal’s growth story: digital sales now account for roughly 61% of total revenue, reflecting a steady shift toward automated ordering, eBusiness platforms, and integrated vending solutions. That digital penetration helps the company scale distribution while improving customer stickiness.

Daily growth and product mix nuance

Behind the headline, daily sales growth moderated to about 2.8% year-over-year, down from September’s pace. Regional splits showed stronger growth outside the U.S. and continued variability across product lines. Fasteners—a historic bellwether for industrial activity—remained under pressure with a roughly 2% decline year-over-year, though that is an improvement versus deeper declines reported in prior months. Safety products, heavy manufacturing supplies, and non-residential construction items posted healthier gains, helping offset softness in traditional fastener demand.

Reporting changes: Why granular OEM and MRO data matters

Fastenal announced it will provide a more detailed breakdown of revenue, separating OEM and MRO channels and leveraging improved customer-master analytics. For investors and analysts this is like switching from a zoomed-out map to a GPS: it provides clearer routing for how growth is being generated. Historically, blended reporting can obscure whether gains are cyclical (tied to manufacturing investment) or recurring (driven by ongoing MRO replenishment). The new disclosures are expected to begin in the current quarter and should allow for better forecasting of durability and margin dynamics across segments.

Implications for FAST stock

Three practical investor takeaways emerge: first, solid aggregate sales reduce near-term downside risk to revenue expectations; second, rising digital revenue and vending/automation deployments support margin resilience as order processing costs fall; third, the clearer OEM/MRO split will help investors determine sensitivity to industrial capital expenditure cycles versus steady replacement demand. In short, the company’s reporting changes could reduce earnings-model uncertainty and narrow analyst estimate dispersion.

Putting the update into context

The picture Fastenal painted is neither uniformly rosy nor deeply concerning. The firm benefits from a diversified product mix and a mature digital platform that together smooth revenue volatility. At the same time, the persistence of fastener weakness suggests some end-user caution in certain manufacturing niches. For disciplined investors, the new disclosure regime should make it easier to separate transient shifts from structural trends.

Conclusion

Fastenal’s October performance—strong headline growth, slower daily momentum, and a meaningful commitment to more granular OEM and MRO reporting—represents a concrete step toward improved visibility for shareholders. The combination of a high digital sales share and better segment detail should help investors evaluate FAST stock with greater precision as the company moves through the current quarter.