Ball Corp: Q4 Strength, Benepack Buy Expands Reach

Mon, March 23, 2026Ball Corp: Q4 Strength, Benepack Buy Expands Reach

Introduction

Ball Corporation’s recent corporate update and quarterly results reinforce the company’s position as a leading aluminum-packaging manufacturer for beverages, personal care, and household goods. Results released in early February and subsequent executive commentary over the past week highlight meaningful cash generation, capacity expansion through an 80% acquisition of Benepack, and steady volume gains—tempered by commodity-premium costs.

Financial and operational highlights

Profitability and cash generation

Ball reported solid earnings for full-year 2025, with comparable diluted EPS and a Q4 showing that underscored resilient demand. Free cash flow reached a record near $1 billion for the year, allowing the company to return about $1.54 billion to shareholders via dividends and share repurchases. Management reiterated guidance for 2026 free cash flow above $900 million—signalling continued emphasis on cash returns and balance-sheet flexibility.

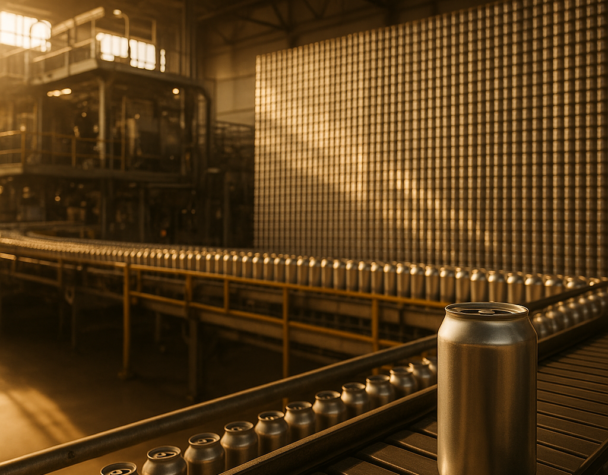

Shipment and volume trends

Shipment volumes rose modestly across regions: total aluminum-packaging shipments rose roughly 4% for the year and accelerated in Q4. North & Central America, EMEA, and South America each posted mid-single-digit volume gains, driven by beverage demand and capacity utilization improvements. Ball’s commentary pointed to seasonal tailwinds—high-profile events later in 2026—that could further support beverage can usage.

Strategic expansion: Benepack and new capacity

Benepack acquisition amplifies European footprint

The acquisition of an 80% stake in Benepack, a European packaging supplier, bolsters Ball’s presence in key markets and adds finishing and can-end capabilities in Belgium and Hungary. This deal accelerates Ball’s strategy of closer-to-customer production, reducing logistics complexity and better matching capacity to demand pockets.

U.S. capacity and plant projects

Ball is also investing in North American capacity, including a new Oregon facility slated to start up in the second half of 2026 with startup costs in the tens of millions. Management noted North American capacity constraints in places, and the new buildouts aim to relieve bottlenecks and capture growth from onshoring and regional beverage demand.

Risks, sustainability, and cost dynamics

Aluminum premiums and tariff effects

While Ball sees limited direct tariff exposure, it faces elevated input-cost pressure from regional aluminum premiums—often referenced as the Midwest Premium—which can squeeze margins if not offset by pricing, mix, or productivity gains. The company is managing these pressures through local sourcing and closer-to-demand manufacturing.

Recycled content and ESG progress

Ball reported increases in recycled-content metrics—reaching mid-70s percentages for beverage packaging—progress toward its 2030 targets. Higher recycled content and domestic production help lower lifecycle emissions and reduce exposure to some commodity swings over time.

Conclusion

Ball’s most recent disclosures combine disciplined cash returns, concrete capacity moves, and improving utilization metrics. The Benepack acquisition and U.S. plant investments provide tangible operational upside, while record free cash flow supports shareholder distributions and strategic flexibility. Near-term risks center on aluminum-premium volatility, but the company’s onshoring and recycling initiatives position it to manage those headwinds while capitalizing on steady beverage and packaging demand.